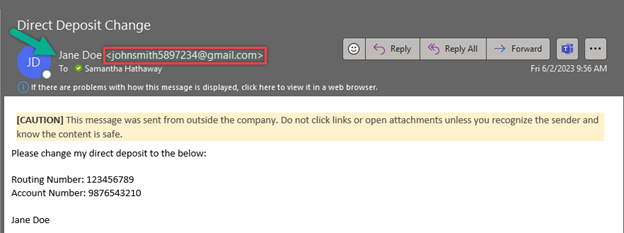

Background

Connecticut is the latest addition to a handful of states implementing state-sponsored retirement programs for private sector employers. MyCTSavings is the offering created by the Connecticut Retirement Savings Authority (CRSA) to provide a retirement vehicle for private sector employees whose employers do not already offer a qualified retirement savings plan for their employees. As explanation for the new requirement, the CRSA estimates that approximately 600,000 Connecticut employees do not have access to employer-sponsored retirement plans.

The program administrator is Vestwell State Savings, LLC, dba Sumday Administration.

Which employers are subject to this new program?

Through MyCTSavings, all private sector employers in the state with five (5) or more employees (each of whom has been paid more than $5,000 in the calendar year) are required to register and facilitate the program, unless they qualify for an exemption.

The CRSA has stated that it will be contacting all private Connecticut employers when it is time to register and will provide a MyCTSavings Access Code with the notification. Employers will require this Access Code along with their federal EIN in order to register. Employers can access the link for registration here.

Employers who already offer a qualified retirement savings plan, can apply for an exemption using this same Access Code. Eligible employer-sponsored plans include: “plan[s] qualified under Internal Revenue Code sections 401(a) (including a 401(k) plan), qualified annuity plan under section 403(a), tax-sheltered annuity plan under section 403(b), Simplified Employee Pension plan under section 408(k), a SIMPLE IRA plan under section 408(p), or governmental deferred compensation plan under section 457(b). It does not include payroll deduction IRAs.” Employers can access the link to certify their exemption here.

While registration for all eligible private sector employers in Connecticut commences April 1, 2022, the deadlines for registration will be implemented gradually in three waves based on the size of the employer as shown in the graphic[1] below provided by the CRSA.

Notably, in a March 31, 2022 article about the program from CBIA (Connecticut Business & Industry Association), there were reports that “Numerous employers report receiving mailings from the state with incorrect or misleading information, including notices warning they have missed the registration deadline.” Employers should review the materials from the CRSA carefully when received. The first registration deadline occurs on June 30, 2022, and is applicable to employers with 100 or more employees.

Are there financial costs for employers associated with the program?

There are no fees associated with employer facilitation of the program, and employers are not required nor permitted to contribute to the program. However, if an employer fails to register, or fails to timely remit payroll deductions on behalf of its employees, there is the possibility that they could be assessed penalties.

While employer facilitation of the program is mandatory (in the absence of an exemption), employee participation is voluntary. Employees are automatically enrolled during the employer registration process and must choose to remain enrolled or to opt out within 30 days. Should they opt-out during this initial period, then their account will not be activated, and no payroll deductions will be taken.

The financial costs for employees (in addition to contribution amounts) include an annual asset-based fee of 0.22% for investment management, as well as an account fee of $26.00 charged and payable in $6.50 installments per quarter.

Employer Responsibilities

Once registered, employers must connect their company bank account, provide a list of employees and enter payroll information. After 30 days have passed, employers will update employee contribution rates within their payroll, and contributions will begin automatically with the next payroll. Employers will be required to maintain current and up-to-date contribution rates and employee rosters. For employees who opt-out of the program after the 30-day notification period, the employer will be notified by the CRSA to stop payroll deductions, and any deductions that may have been made may be withdrawn by the employee.

An Employer Registration Checklist can be found here.

After employers have registered, they can provide notice to their workforce of the program, its benefits, and an employee’s ability to opt-out of participation in the program with the following Auto-Enrollment Notification.

The CRSA will monitor each employee account and notify employers when to stop contributions when an employee is nearing his/her contribution limit. The CRSA will track only the contributions made through the program, and will not have contribution information to another Roth or traditional IRA that the employee participates in. Employees must monitor their contribution limits across all retirement accounts to ensure IRS annual limit compliance and should consult a tax expert or financial advisor relative to their specific circumstances.

Employers do not report employee contributions on Form W-2. Per the MyCTSavings Employer FAQs, “the IRA trustee for the MyCTSavings program will file “Form 5498, IRA Contributions Information” with the IRS (as needed for your employees) and will send employees a copy for their records, no later than May 31.”

What type of retirement plan is MyCTSavings?

MyCTSavings is a Roth IRA, which means that contributions are made with post-tax dollars. The default employee contribution rate is 3% of an employee’s gross wages, up to the annual maximum set by the IRS based on the employee’s modified adjusted gross income (AGI). If an employee’s modified AGI exceeds certain IRS maximum thresholds, with consideration for filing status, then an employee’s maximum contribution may be reduced, or the ability to contribute may be eliminated. Employees have the ability to adjust or change their contribution amounts and investment options, in accordance with the program rules. More information on investment options and contributions can be found here and here.

Employees must be at least nineteen (19) years of age, be paid in Connecticut by their employer, and have been employed for at least 120 days. There is no waiting period, but if an employee works for an employer for less than 120 days, an employer may not enroll him/her. Business owners or shareholders are permitted to participate in the program as Savers if they meet the definition of employee for tax purposes.

The MyCTSavings website has a multitude of information for employers and employees alike and employers are encouraged to continuously check back periodically for updates.

[1] https://myctsavings.com/employers/program-details

Disclaimer: The information contained herein is not intended to be construed as legal advice, nor should it be relied on as such. Employers should closely monitor the rules and regulations specific to their jurisdiction(s) and should seek advice from counsel relative to their rights and responsibilities.

Disclaimer: The information contained herein is not intended to be construed as legal advice, nor should it be relied on as such. Employers should closely monitor the rules and regulations specific to their jurisdiction(s) and should seek advice from counsel relative to their rights and responsibilities.